The gap between what Marshmallow's ads can say and what a typical insurer's ads can say isn't a creative gap. It's a data gap. Cohort-specific average savings figures, calculated per policyholder segment, compliant under FCA financial promotions rules, served dynamically at scale - that only exists if the data infrastructure underneath it works. Most performance marketing teams are operating with incomplete signals, slow creative pipelines, and attribution gaps that make this kind of precision impossible.

Marshmallow appears to have solved it. Here's what 18 months of their Meta ad library reveals about how they did it - and what it means for anyone building paid acquisition in regulated financial services.

The core insight that makes everything else possible

Before the data, there was a product insight: most UK insurers penalise drivers by ignoring driving history earned outside the UK. Marshmallow's product solves this. Everything in their paid strategy flows from that single differentiator - but the differentiator only becomes a paid acquisition advantage when you have the data to prove it, at the level of specificity that makes someone stop scrolling.

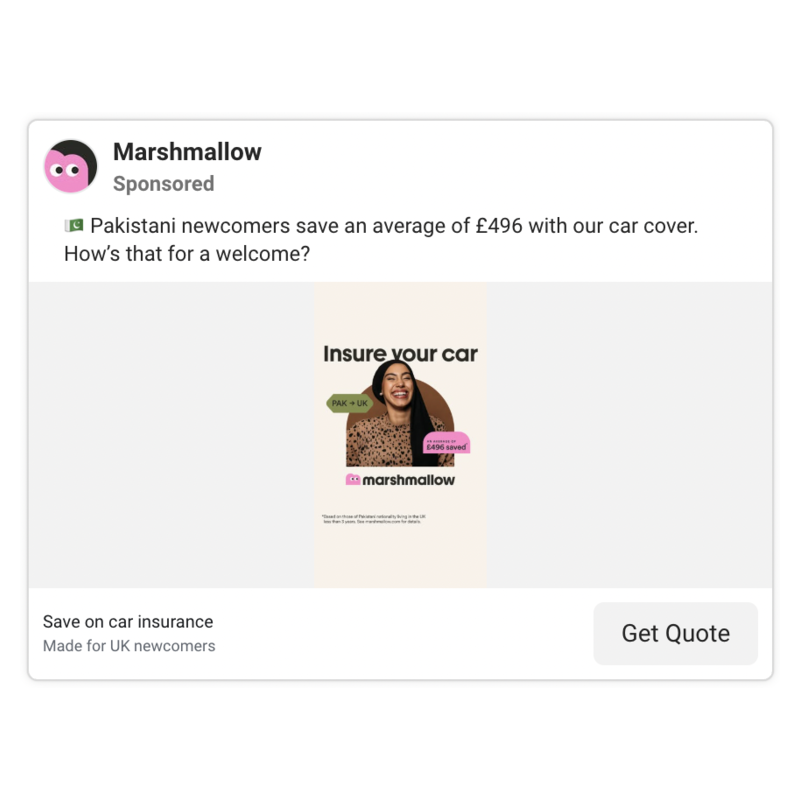

"Save money on car insurance" doesn't stop anyone. "Drivers like you save an average of £358 with our UK car cover" does. The difference between those two statements is data infrastructure.

What's worth noting is that this isn't just a creative decision. It's a signal about the maturity of the entire acquisition system. To get a specific, defensible savings figure into regulated financial advertising, three things have to be true simultaneously: the data exists and is accurate, the analytics function can calculate it correctly, and compliance will sign it off under FCA financial promotions rules. That alignment is harder to achieve than it sounds. When you see it in an ad, you're seeing the output of an infrastructure problem that's already been solved. And as the ad library shows, once that infrastructure exists, it compounds.

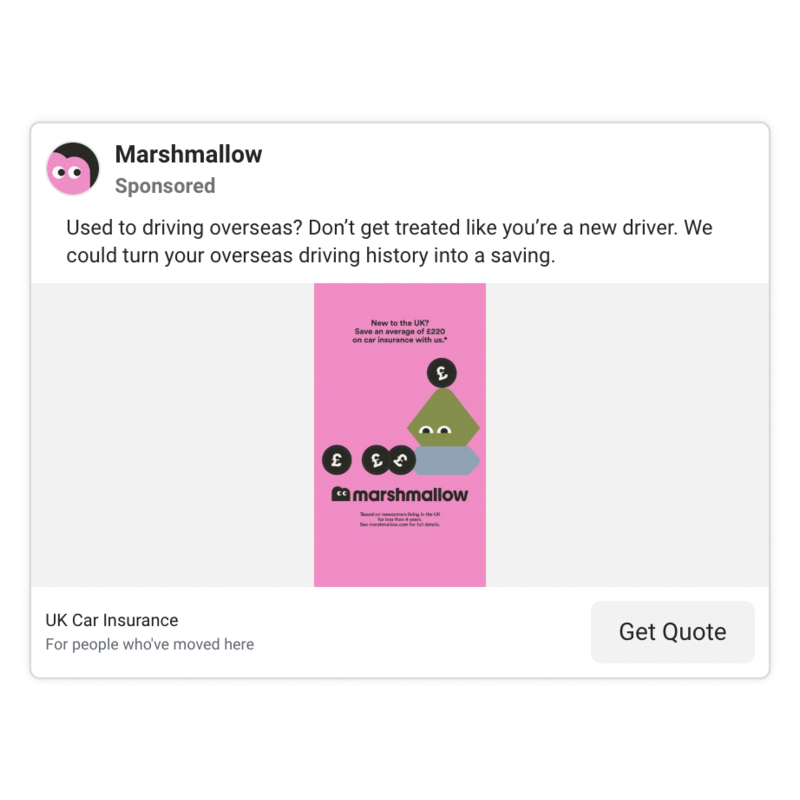

Stage 1: Establishing the insight (Feb 2024 - Aug 2025)

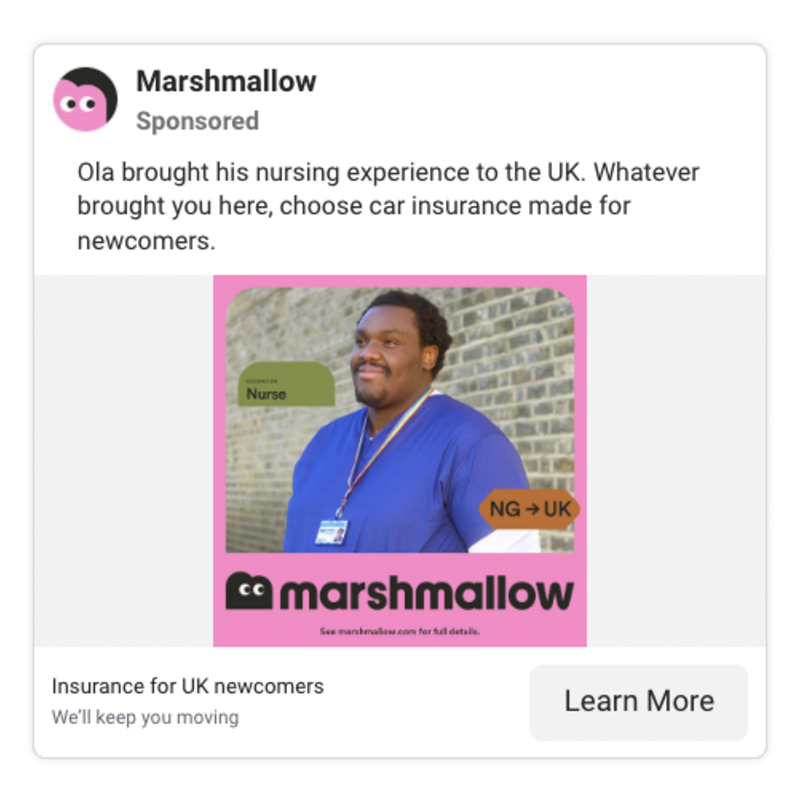

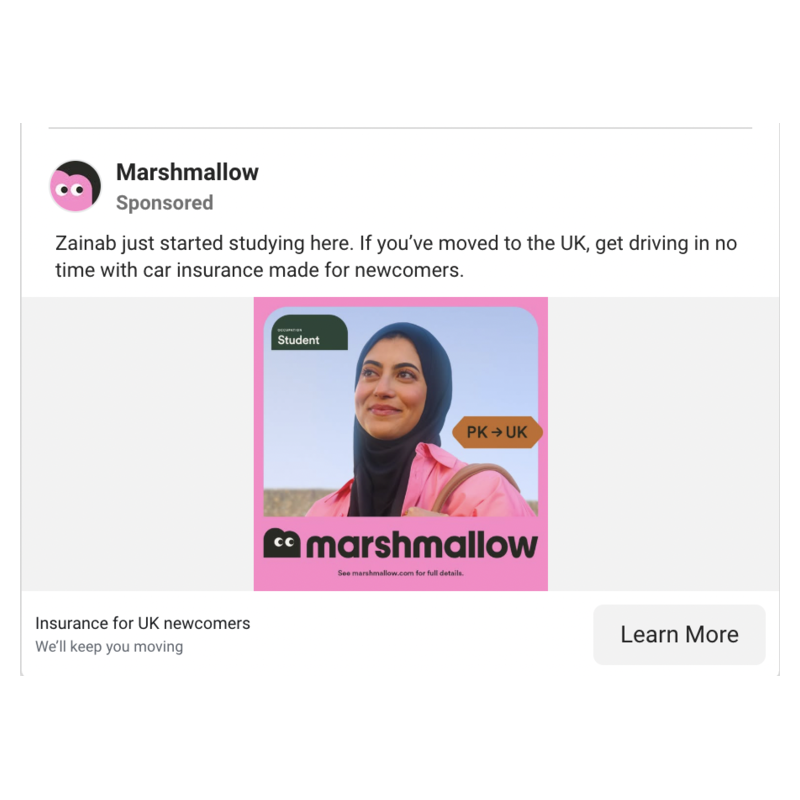

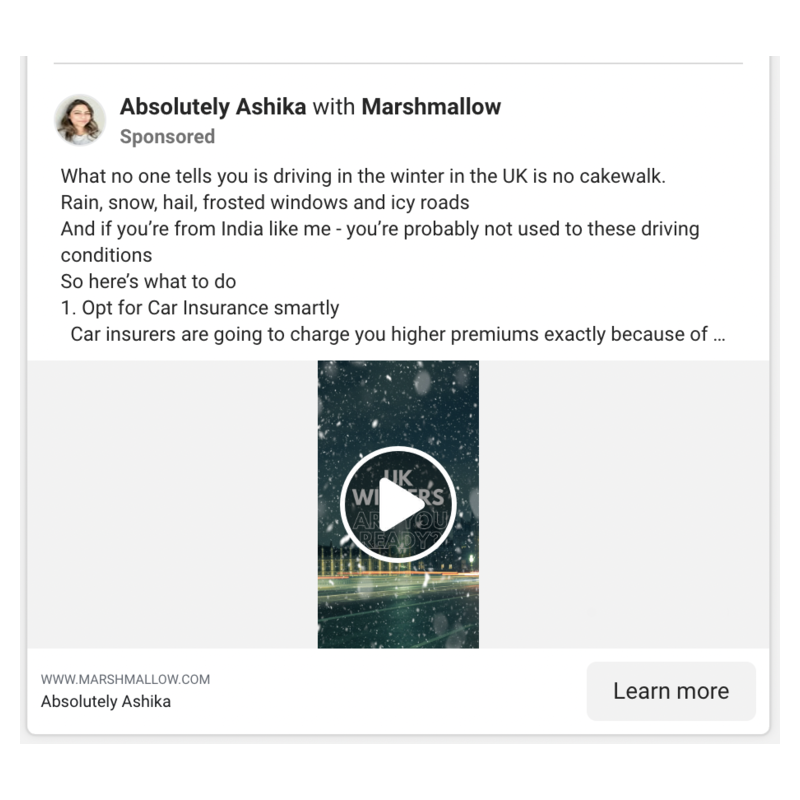

The earliest ads in the library are awareness-led. Named personas represent archetypal newcomer journeys, with origin-to-destination visual cues making the targeting visible in the creative itself. The CTA is "Learn More," not "Get Quote." This is brand work - building recognition and trust with an audience before asking them to convert.

But the strategic intent is already visible. The segmentation logic is built into the creative rather than hidden in the targeting layer. The audience recognises themselves in the ad. That's a deliberate choice, and an early signal of where the system is heading. The data infrastructure to make it precise doesn't exist yet - but the creative logic that will eventually be powered by it does.

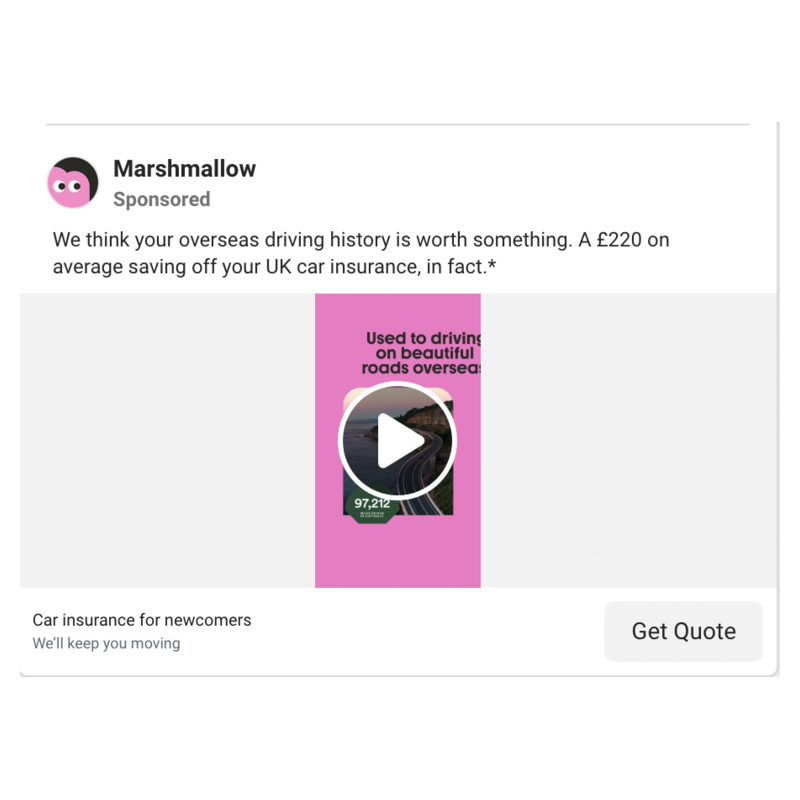

Stage 2: The shift to performance - and the data starting to show (Sep - Nov 2025)

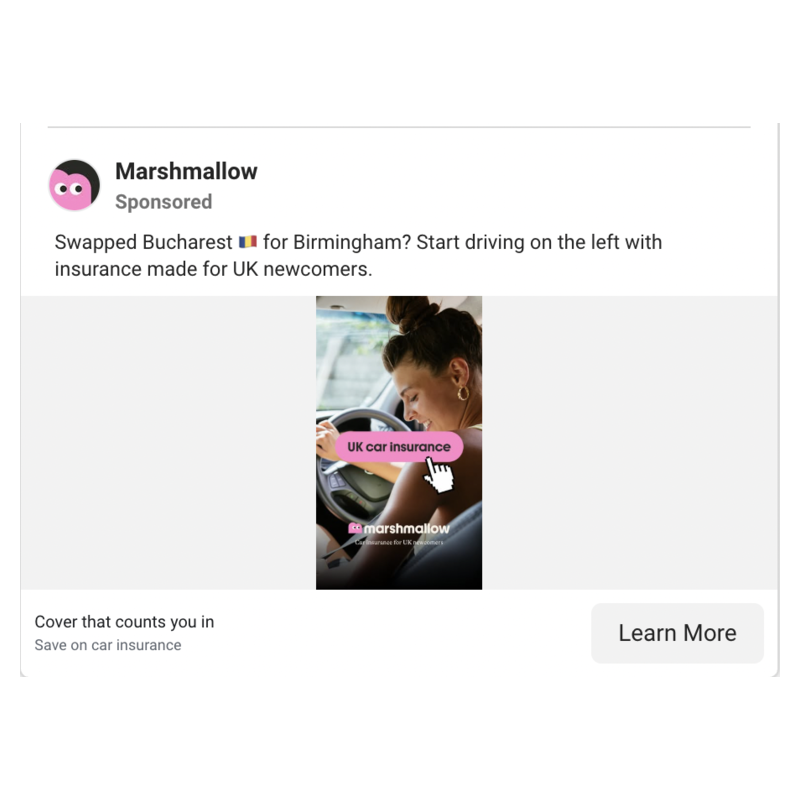

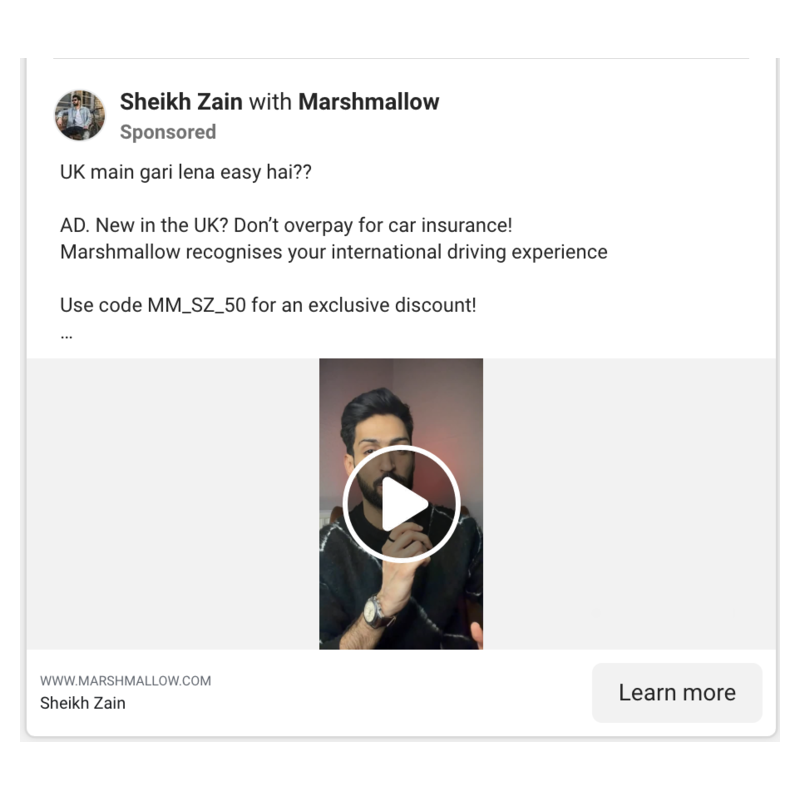

By September 2025 the messaging tightens into direct response. The structure becomes "most insurers do X, we do Y" - a challenger frame that works when the product difference is real and provable. "Get Quote" replaces "Learn More." Creative volume increases significantly, with some creatives running 8-15 ad variants simultaneously. The account is scaling and testing, which means the measurement infrastructure is mature enough to interpret what it learns.

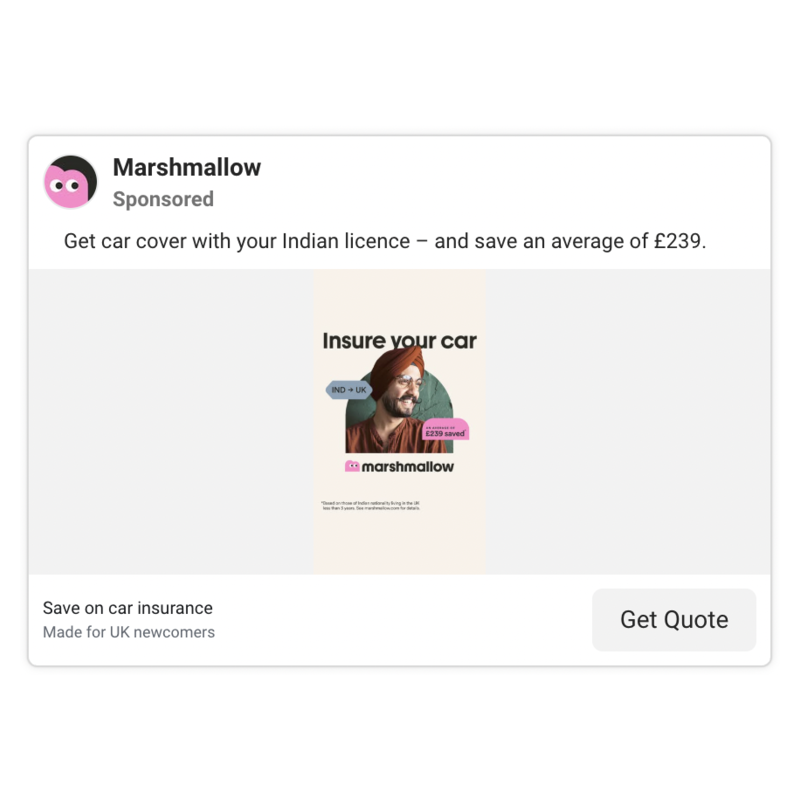

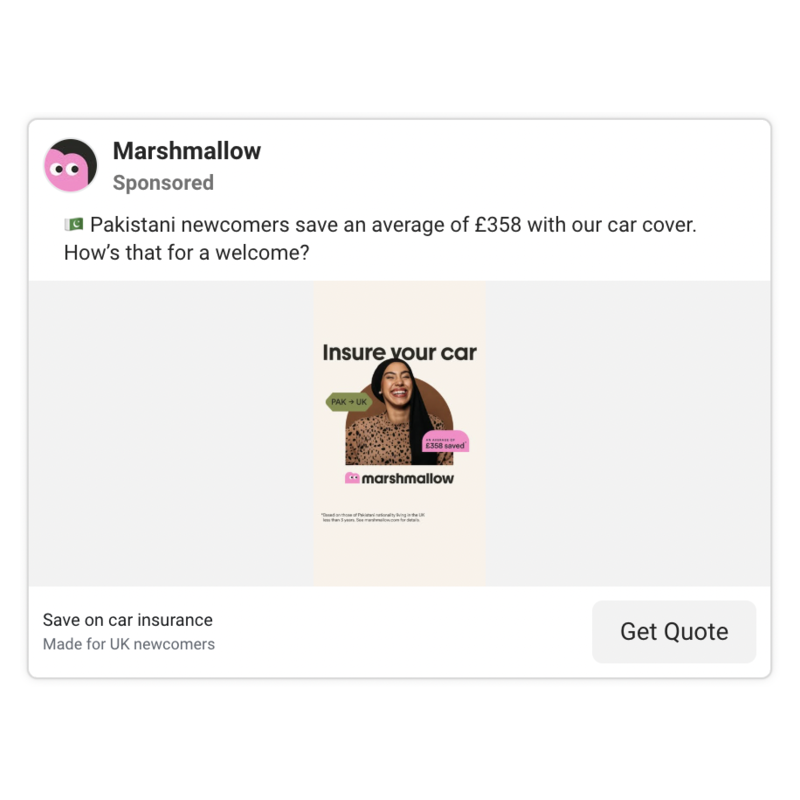

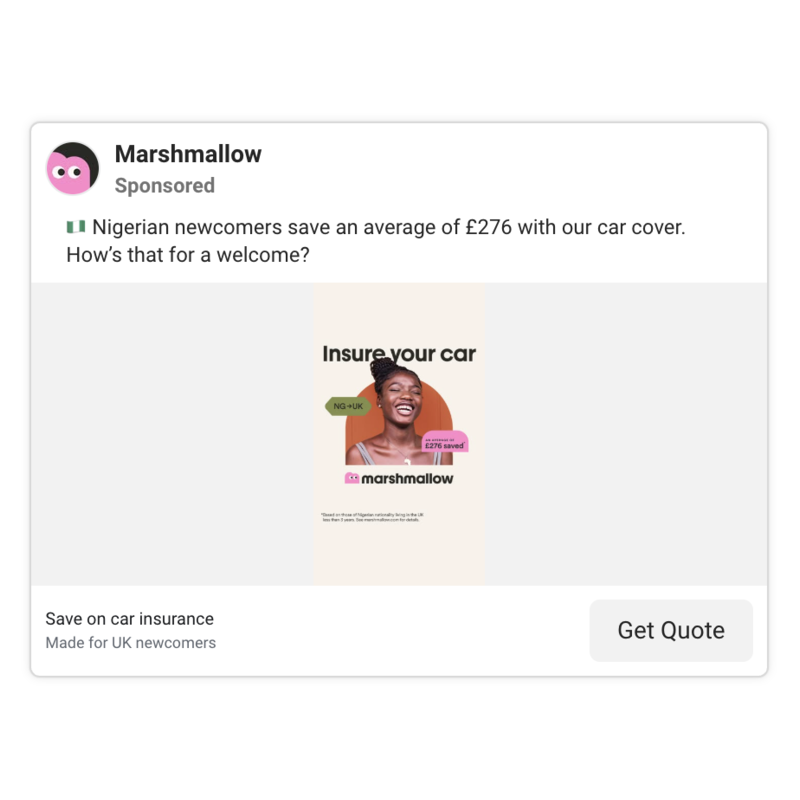

Then in October 2025, the data infrastructure becomes visible in the creative for the first time. Cohort-specific average savings figures appear in ad copy. These aren't estimates. They're calculated from actual policyholder data, segmented by meaningful cohort characteristics, and published under FCA financial promotions rules.

This is the moment the earlier brand investment starts to pay off. The audience recognises themselves from months of awareness creative - and now the ad can prove, in precise financial terms, what the product is worth to someone in their situation. The creative and the data have caught up with each other.

It's also the moment you can start to see the outline of what the system could eventually become.

Stage 3: Cultural specificity and the influencer layer (Jan - Mar 2026)

January 2026 brings a creative evolution that goes beyond segmentation into genuine contextual specificity. The copy references driving conditions and experiences that are meaningfully different across the segments Marshmallow serves - not just who someone is, but what driving actually felt like before they arrived in the UK. This level of detail signals that the qualitative research infrastructure is maturing alongside the quantitative one. The system is getting smarter about its audience in multiple directions simultaneously.

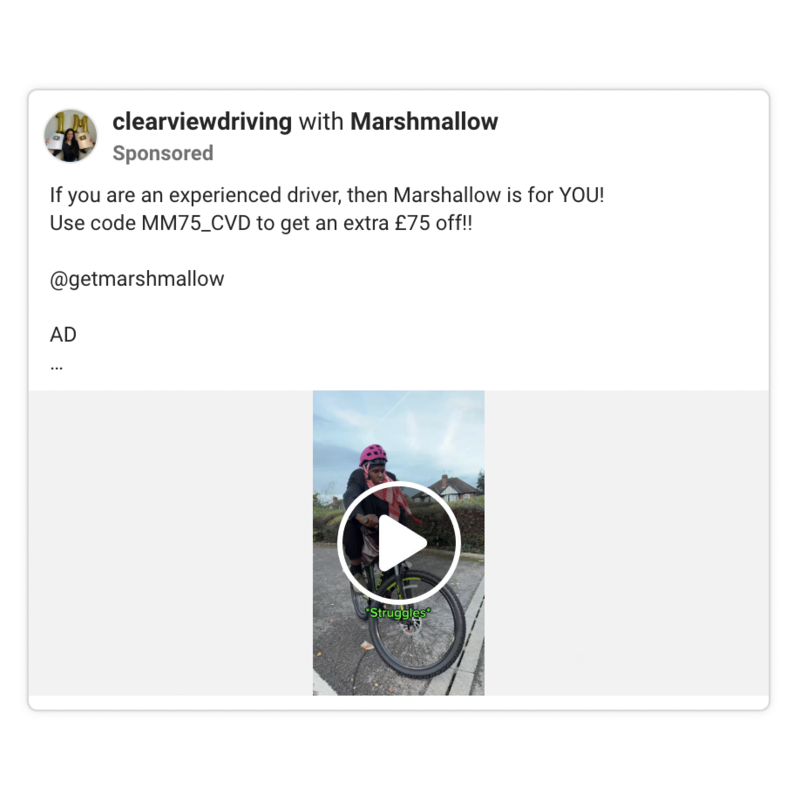

The influencer layer appears at scale in February 2026, and the mechanics are worth examining carefully. Each creator is matched not by follower count or broad demographic fit, but by their relevance to a specific context cluster within Marshmallow's audience. Each carries a unique discount code - individual conversion attribution baked in from the start.

The structural point is this: Marshmallow has built a parallel paid social channel using creators as a targeting layer, with the same performance rigour applied to influencer spend as to direct brand ads. It's not a social strategy bolted onto a performance strategy. It's a unified acquisition system with multiple creative surfaces, all feeding back into the same measurement framework.

Creative volumes at this stage reflect the maturity of the whole system. Single direct brand creatives are running 22 ad variants simultaneously. That's an account testing aggressively - and one that has the infrastructure to act on what it learns. Which raises the question of what that infrastructure could look like if it were pushed further.

Stage 4: Peak complexity and the May 2026 pause (Apr - May 2026)

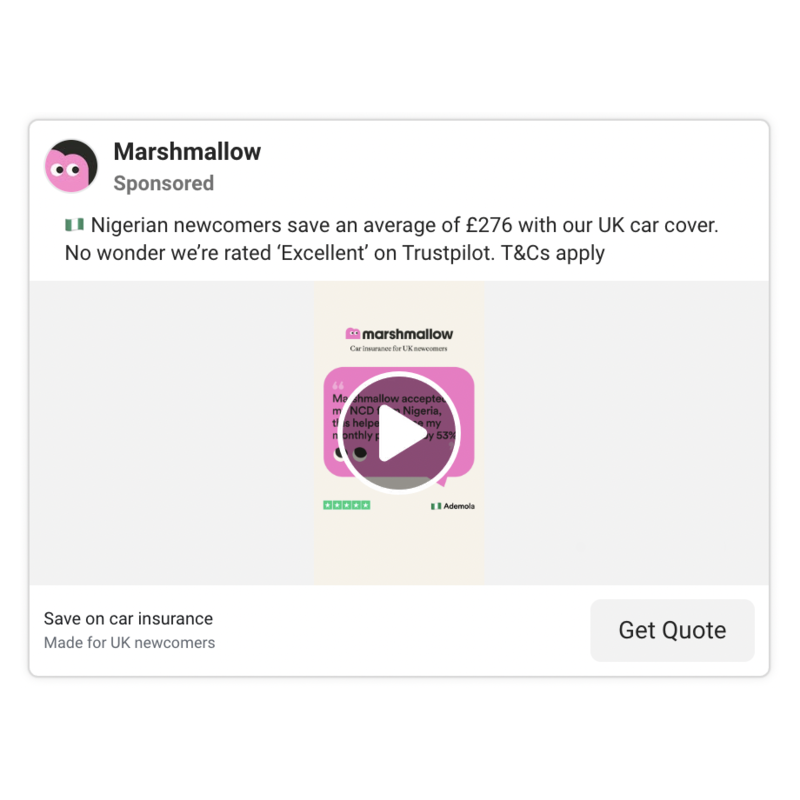

April 2026 represents peak creative complexity. Cohort-specific savings figures now carry Trustpilot ratings as an additional social proof layer - a second data point reinforcing the first. Some creatives have 25-26 active variants. The creative matrix covers: segment × savings figure × format (static/video) × copy angle (savings/simplicity/social proof). That's a multivariate testing framework running in production at scale - and it only generates useful signal if the measurement layer underneath it is working correctly.

Then in mid-May 2026, everything goes inactive.

What the pause probably means

A brand running 25+ ad variants on a single creative doesn't pause for creative fatigue. More likely explanations:

Budget cycle reset. May is an unusual time to pause unless it marks the end of a financial period or a reallocation ahead of a new planning cycle. With Marshmallow mentioned alongside other UK fintechs as a potential IPO candidate, there may be pressure to demonstrate marketing efficiency rather than raw spend volume going into a new period.

A platform strategy shift. The creator programme they've built is a parallel acquisition channel with performance attribution built in. It's possible budget is rotating toward that channel and away from direct brand ads - particularly if creator-led content is outperforming on CAC.

A creative platform reset. Eighteen months of the same core product insight eventually reaches saturation within the addressable audience. The pause may precede a new campaign direction - the next strategic layer after they've extracted maximum value from the current segmentation approach. The interesting question is what comes next: do they go deeper on the same audience, or broader as the customer base matures beyond the newcomer segment?

Whatever the reason, the pause is a useful moment to ask a bigger question. Marshmallow have built something genuinely sophisticated. But the ad library is only the visible surface. What would this system look like if the infrastructure underneath it were pushed to its logical conclusion?

What a fully realised version of this system looks like

Layer 1: Signal engineering

Right now, Marshmallow's Meta campaigns are almost certainly optimising toward a standard conversion event - a completed quote, a policy purchase. That's table stakes. But the policyholder data they're sitting on makes a much richer signal possible.

The first step is getting first-party data flowing correctly. A properly implemented server-side GTM stack - capturing quote behaviour, coverage tier selection, payment method, referral source - feeding back to Meta via the Conversions API dramatically improves match rates and restores signal quality that browser privacy changes have degraded. Most insurers haven't done this properly. It's the foundation everything else depends on.

The more interesting step is what you do with the policyholder data itself. Marshmallow knows, from their existing book, which customer profiles generate high LTV - low claims frequency, multi-year retention, willingness to add extras. That data can be used in three ways simultaneously: as a value signal fed into Meta's bidding algorithm to train it toward high-LTV acquisitions rather than just conversions; as a seed audience for Lookalike generation, where the model is finding people who look like your best existing customers rather than your most recent ones; and as a predictive signal, where early behavioural indicators during the quote flow are used to score incoming leads in real time and adjust bid values dynamically.

Each of these is a distinct engineering problem. Getting all three working in parallel, with clean data pipelines and measurement that can tell you which signal is actually driving performance, is where most teams hit a wall.

Layer 2: Creative automation

In parallel, a platform like Hunch solves a different problem: how do you produce and serve personalised creative at the scale Marshmallow's segmentation logic demands, without a creative team manually producing hundreds of variants?

The answer is template-driven creative automation. You build a master template - the structural and visual framework of the ad - and connect it to a data feed that populates the variables: the cohort identifier, the savings figure, the social proof element, the CTA. The platform generates the full creative matrix automatically. What currently requires manual production of 25-26 variants per creative becomes a data feed update.

The data feed is where it gets interesting. It needs to be connected to live policyholder data - so that the savings figures in the creative are always current, always accurate, and always defensible under FCA financial promotions rules. That's not a marketing operations problem. That's a data engineering problem that marketing has to own.

Layer 3: What happens when you run both simultaneously

This is the question worth asking, because the answer isn't obvious.

Signal engineering and creative automation are solving personalisation at different layers. Signal engineering tells the algorithm who to find and what to optimise toward. Creative automation determines what that person sees when the algorithm finds them. Run independently, each makes the system better. Run together, with the right architecture, they create something qualitatively different.

The closed loop looks like this: your sGTM stack captures rich behavioural signals during the quote flow. Those signals feed into Meta's algorithm, which starts to build a picture of what a high-LTV customer looks like behaviourally - not just demographically. The algorithm uses that picture to find lookalikes. The creative automation platform serves those lookalikes a creative dynamically matched to their predicted cohort characteristics - the right savings figure, the right context, the right social proof - generated automatically from the data feed. The policy is purchased. The new policyholder data flows back into the LTV model, which sharpens the signal, which improves the lookalike, which improves the creative match.

Each cycle makes the system more precise. The creative gets more relevant. The algorithm gets smarter. The CAC comes down not because you spent more, but because the system is learning faster than a manually operated one can.

Why most teams can't build this

The reason this system doesn't exist at most insurers - or most fintechs - isn't budget and it isn't ambition. It's organisational. Building it requires marketing, data science, engineering, and compliance to work as a single function toward a shared outcome. In practice, those teams have different priorities, different timelines, and different definitions of done.

The signal engineering work sits at the boundary of marketing and engineering. The LTV modelling sits at the boundary of data science and finance. The creative automation sits at the boundary of marketing and product. The compliance sign-off on dynamic financial promotions copy sits at the boundary of all of them.

The performance marketer who can operate across all of those boundaries - who speaks the language of data engineering, understands what the algorithm actually needs, and can get compliance to sign off on dynamic creative - is the person who unlocks this. That's a different role than campaign management. It's closer to product ownership of the acquisition system itself.

Marshmallow's ad library suggests they have someone like that. Most of their competitors don't yet.

What this means for performance marketers in regulated financial services

Three things stand out from this analysis that apply beyond Marshmallow.

The best audience segmentation is built into the creative, not hidden in targeting. When your audience sees their specific context reflected in an ad - their situation, their driving history, a savings figure calculated from people like them - the ad does something targeting alone can't. It signals the product was built for them. That's not a media buy. It's a product truth made visible through data.

Data infrastructure is a competitive advantage - and the gap is bigger than most teams admit. The cohort-specific savings figures only work because the underlying data exists, the analytics capability to calculate them correctly is in place, and compliance has signed off on their use in financial promotions copy. The gap between what Marshmallow's ads can say and what a typical insurer's ads can say is really a gap in data infrastructure - not creative ambition. Building the infrastructure is the hard part. The creative follows.

Performance influencer marketing is underused in UK fintech and insurtech. Marshmallow's creator programme works because attribution is tracked individually, creators are selected for contextual relevance rather than reach, and the content achieves specificity that brand creative rarely manages. Most fintech paid teams haven't built this properly - partly because it requires both creative judgment and performance rigour simultaneously, which is an uncomfortable combination for teams organised around one or the other.